True

True

UK Energy Market Analysis - October 2025

Recently, warmer and windier-than-average weather has driven short-term prices lower. However, the absence of gas injections into European storage...

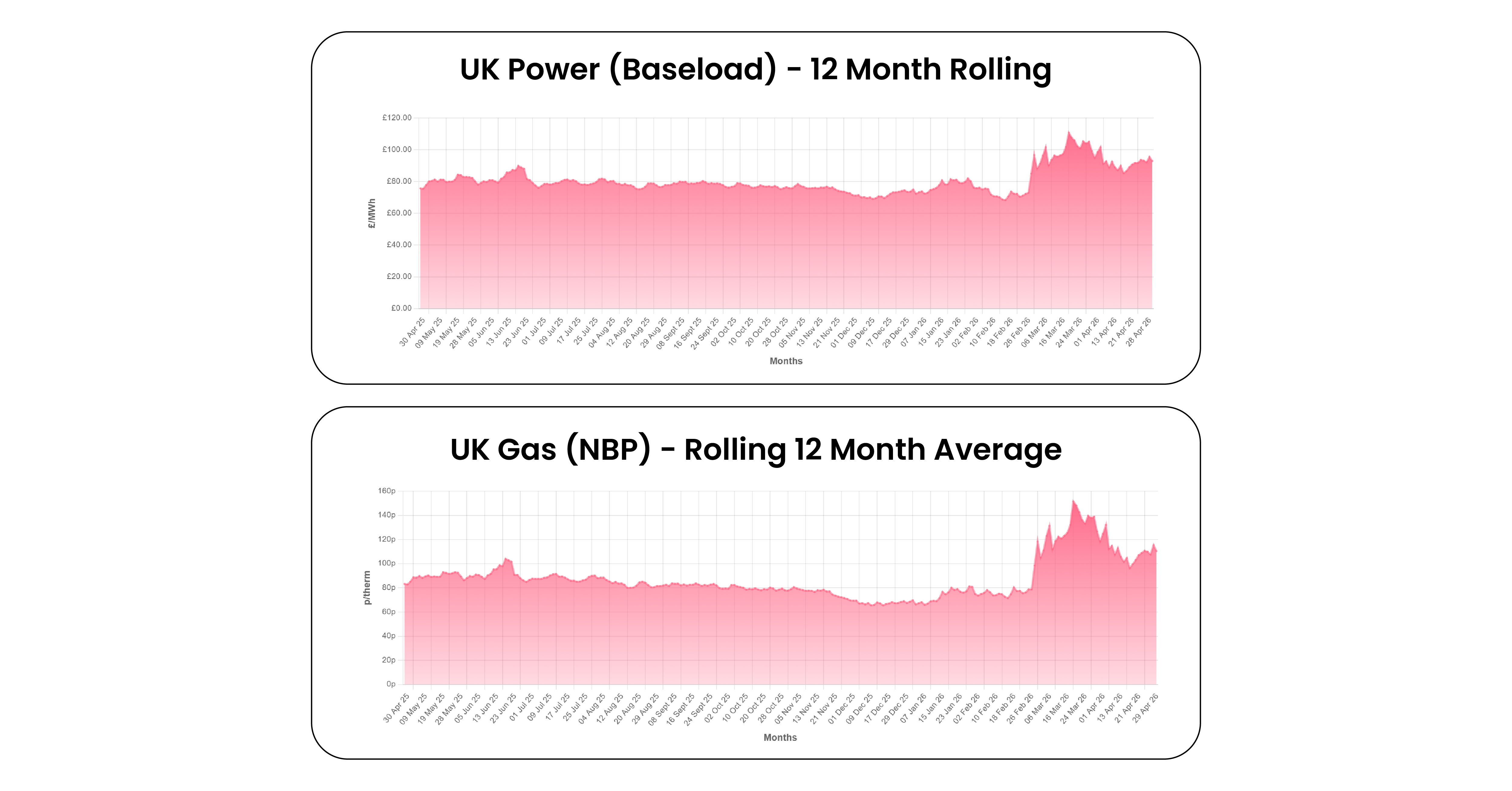

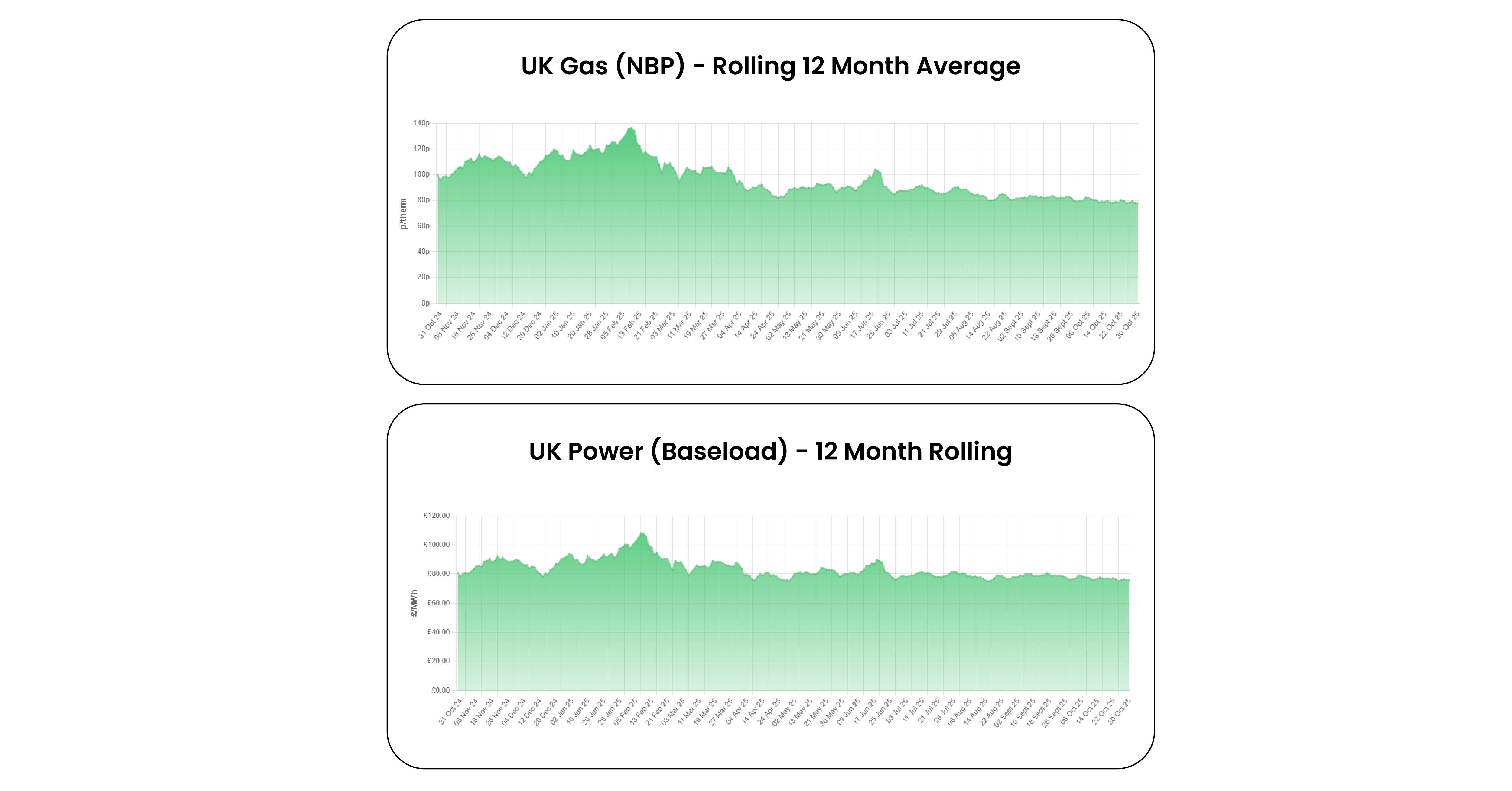

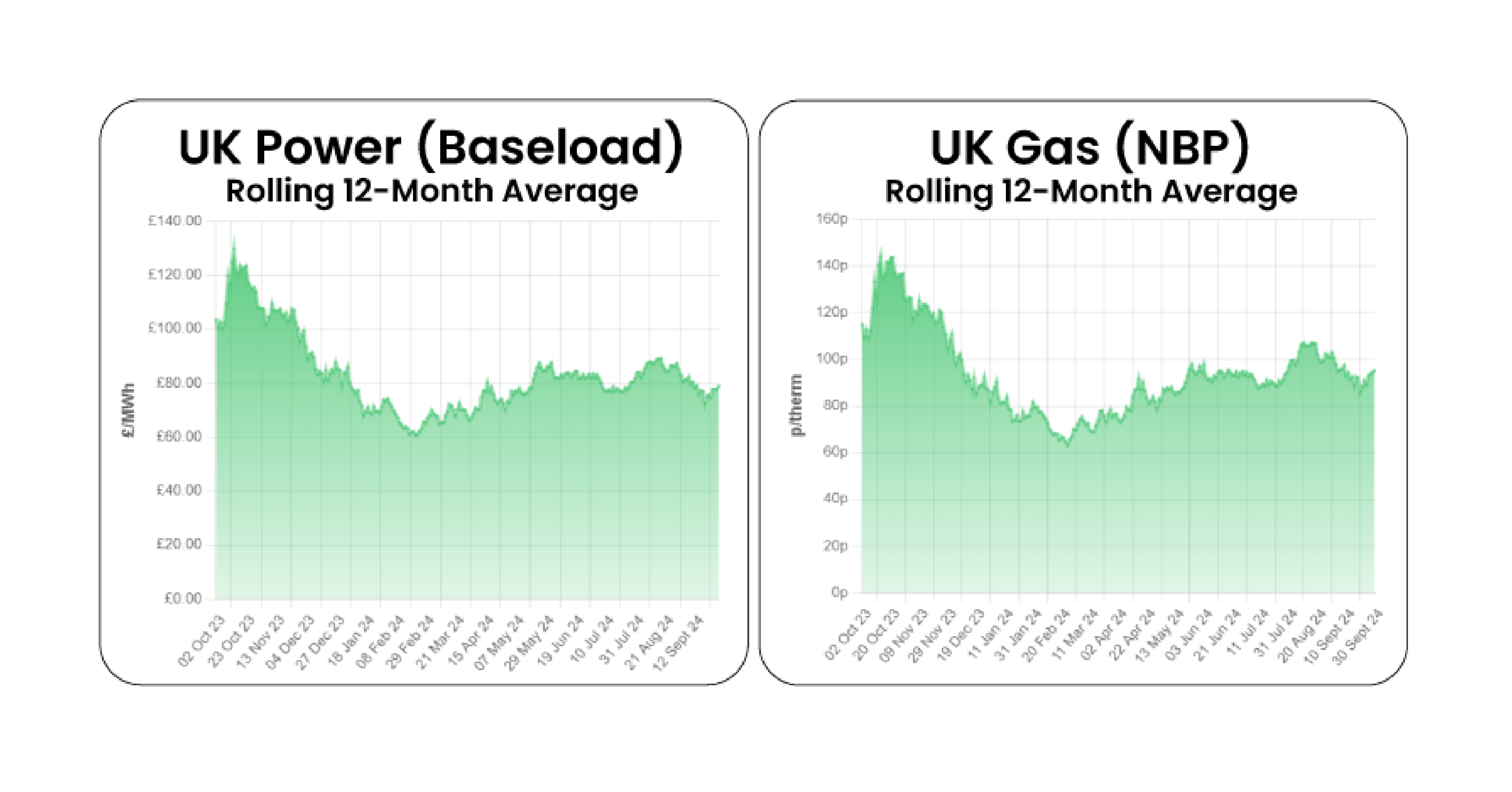

The combination of strong renewable output and low seasonal demand has kept short-term power prices low, particularly in France, where robust nuclear availability is adding further downward pressure: baseload prices for delivery from Friday 24th April to April 30th have averaged €7.74/MWh. By contrast, gas and oil markets have seen a sharp increase in volatility, with Brent briefly spiking to a four-year high of $126.41 on April 30th before correcting by around $10. For now, the Middle East remains the key driver, with risks of renewed military action and potential further damage to Qatari LNG infrastructure continuing to support the risk premium in gas contracts.

Economic Environment

• Both the ECB and the Bank of England have kept interest rates unchanged, signalling a cautious stance as they assess persistent inflation and the outlook for economic growth.

• Germany’s economy ministry cut its growth forecast for 2026 as higher oil and gas prices weigh on economic activity, now expecting output to expand by 0.5%, down from 1.0%, while raising its inflation projections.

• UK inflation rose to 3.3% in March, from 3.0% in February, driven by a surge in petrol prices as higher energy costs linked to the Iran war fed through.

Oil

• Global oil prices have been highly volatile in April, driven by the Middle East conflict and the continued disruption to flows through the Strait of Hormuz. Brent crude traded within a wide $40.25 range over the month, ending around 10% higher.

• The physical oil market remains under acute strain, with the US blockade and Tehran’s restrictions reducing transit to a trickle. Even after accounting for bypass routes such as Saudi Arabia’s East–West pipeline, the net disruption is estimated at around 10 mb/d this month.

• The UAE said it would leave OPEC from 1st May, citing a shift towards prioritising national interests and expanding production capacity. The move marks a significant structural rupture, though the immediate bearish impact is limited due to the ongoing conflict.

Gas

• EU gas demand is set to fall by 8bcm (2.5%) to 314bcm this year, pressured by high prices, persistent geopolitical risk and rising renewable output, according to Kpler. Regionally, northwest Europe is set to decline by 4bcm, southern Europe by 6bcm, while the rest of the EU-27 is expected to see a 2bcm increase.

• Despite the ongoing interruption in LNG exports from Qatar, low demand and strong renewable output have driven a 4.3 percentage point increase in European gas storage levels since 1st April. Inventories are currently 32.2% full, compared with 39.0% at the same point last year.

• Golden Pass has exported its first cargo from the new Texas terminal this month, marking the start-up of Train 1, with Italy previously indicated as the likely destination. The project is only partially operational, with Trains 2 and 3 still under construction, and total capacity expected to reach 18 mtpa once fully online.

• Japan will temporarily increase coal-fired power generation to offset LNG supply disruptions caused by the closure of the Strait of Hormuz. The plan includes suspending for one year the 50% utilisation limit on coal-fired power plants, potentially reducing LNG imports routed via the Strait by 10%.

Power

• European power markets plunged to record negative levels on Sunday as strong renewable output collided with weak demand. France posted its lowest day-ahead baseload price since June 2013 at €-40.83/MWh, while intraday prices dropped below €-400.00/MWh across Germany, France and Hungary, including a low of €-480.01/MWh in Germany.

• The UK government will remove the Carbon Price Support (CPS) tax from April 2028, as expected, citing its reduced relevance following the phase-out of coal generation. Introduced in 2013, the tax is currently set at £18/tonne, and sits on top of the UK Emissions Trading Scheme.

• The European Commission has approved state aid schemes in Germany, Bulgaria and Slovenia to provide temporary electricity price relief for energy-intensive industries. The budgets are €3.8bn for Germany, €334mn for Bulgaria, and €90mn for Slovenia.

• Despite a relatively modest monthly decline of around 6.5%, the Winter 26 NBP gas contract exhibited significant intramonth volatility, trading within a c.37.5 p/th range amid ongoing Middle East uncertainty.

If you would like the latest insights weekly, sign up for our Energy Market Update.

Recently, warmer and windier-than-average weather has driven short-term prices lower. However, the absence of gas injections into European storage...

Global equity markets responded positively to the Federal Reserve’s decision to cut interest rates by half a point in September. This move was...