From Baku to Belém: A Round-Up of COP29 & What To Expect At COP30

COP 29: The ‘Finance COP’

COP 29: The ‘Finance COP’

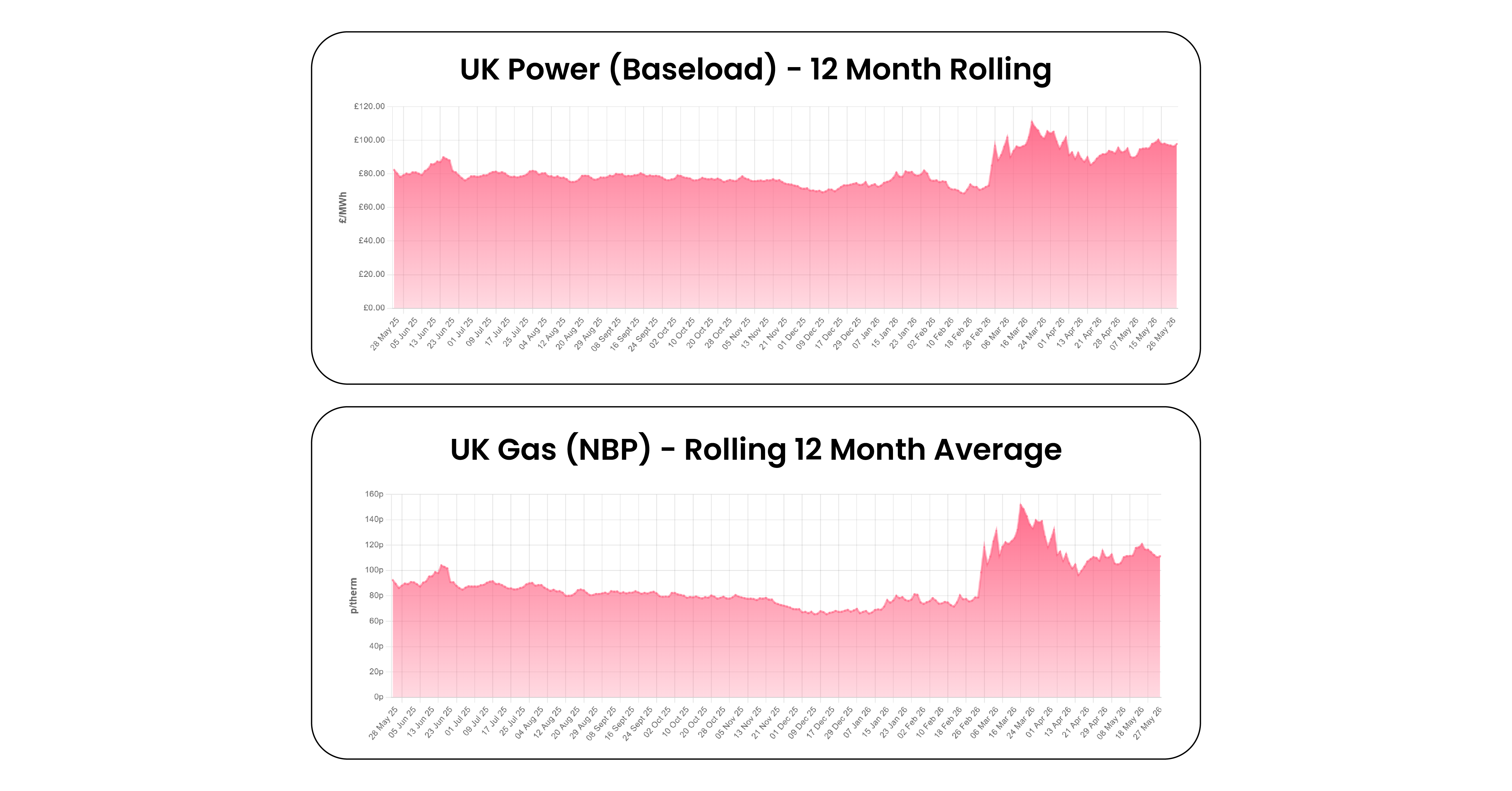

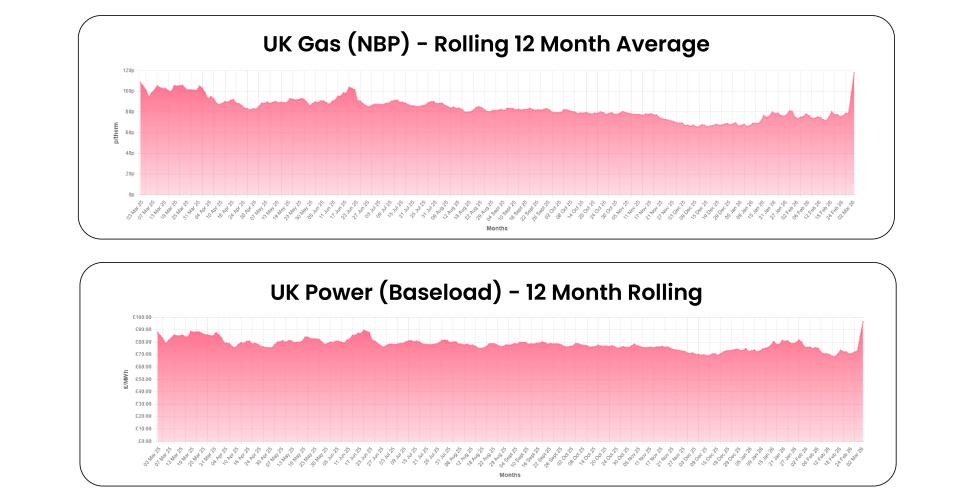

Short-term gas prices weakened this week, with the UK day-ahead gas contract down around 10p week-on-week as heatwave conditions suppressed heating...

1 min read

Gas and oil markets have been extremely volatile this week. For example, the UK April gas contract reached 171.00 p/th on Tuesday morning, more than...