True

True

UK Energy Market Analysis - May 2026

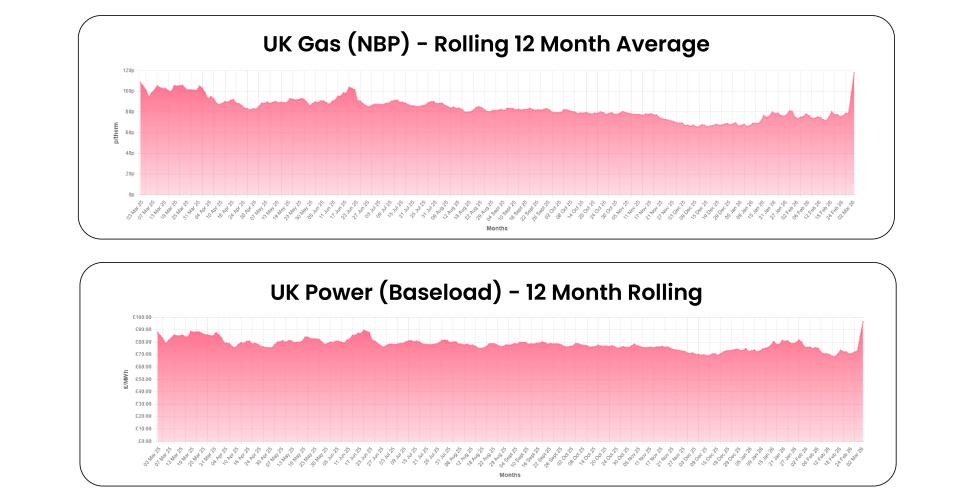

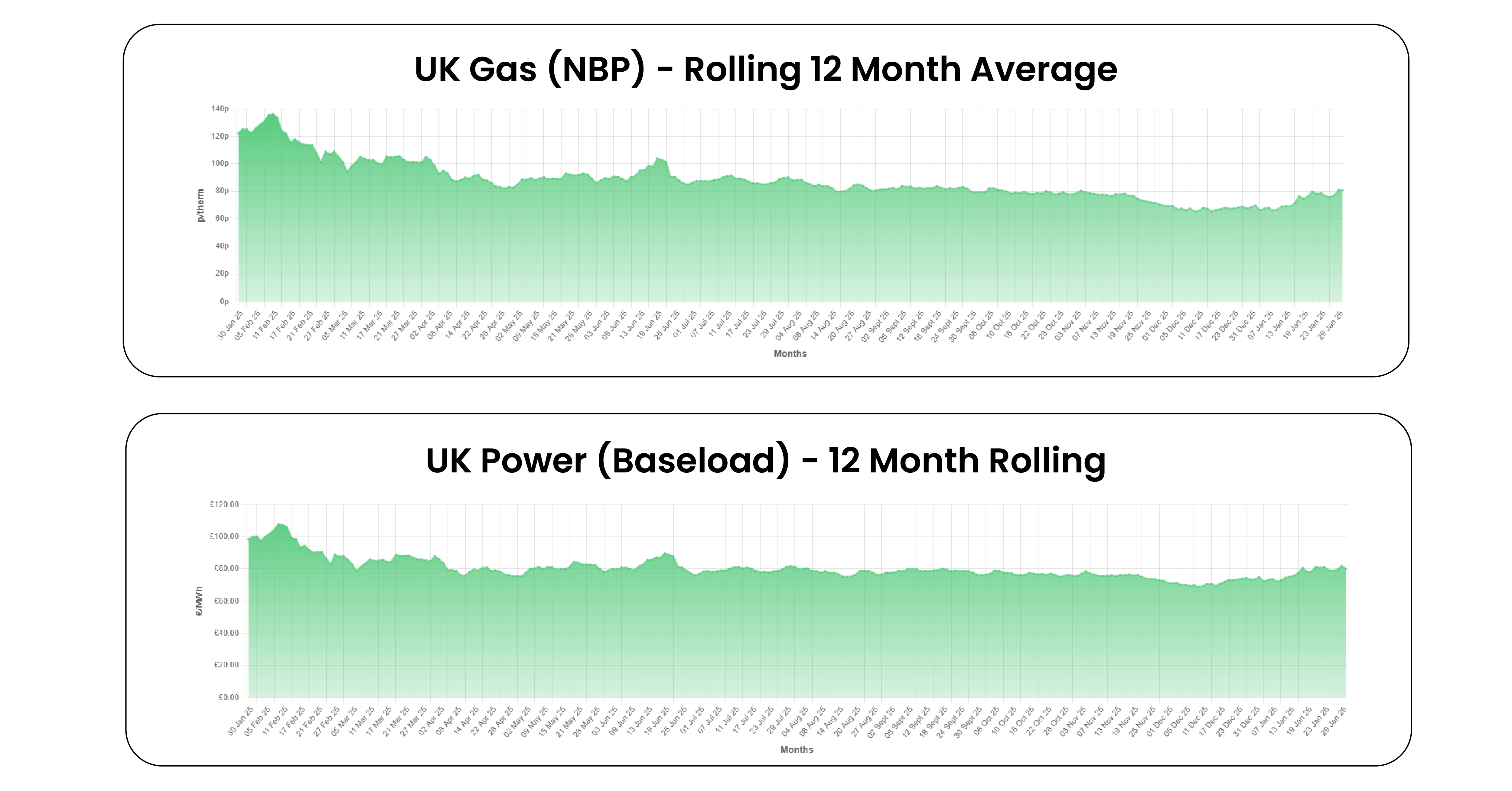

Short-term gas prices weakened this week, with the UK day-ahead gas contract down around 10p week-on-week as heatwave conditions suppressed heating...

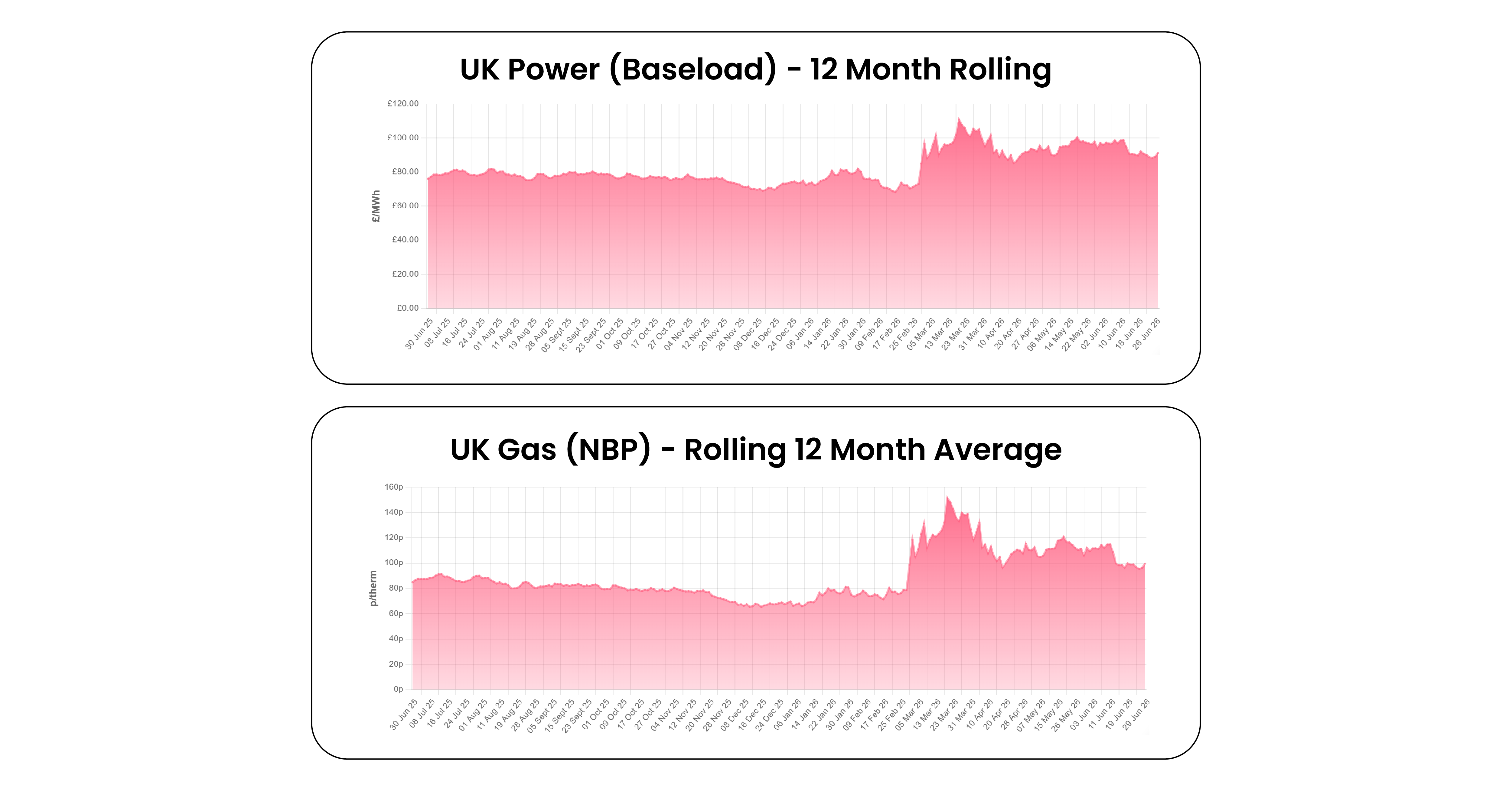

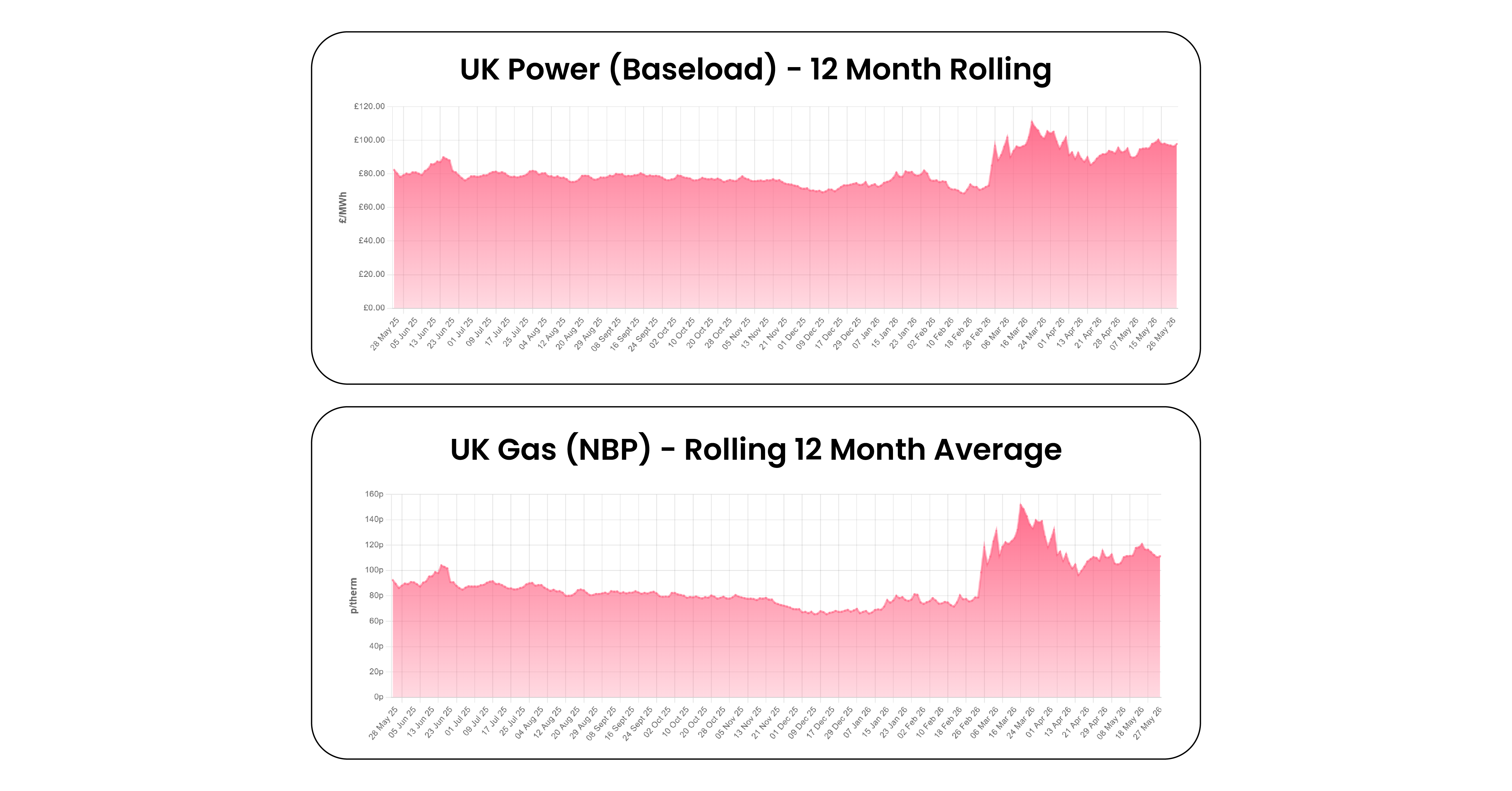

The record-breaking heatwave across Europe lifted cooling demand while simultaneously constraining power supply through weaker wind generation under persistent high-pressure conditions and reduced nuclear output due to river temperature restrictions. This drove prompt power prices sharply higher and boosted gas demand for power generation, with Belgium's day-ahead baseload price reaching €257.55/MWh last week and the UK's reaching £159.10/MWh for delivery on Wednesday 24 June. Despite these short-term market pressures, forward contracts softened as improving LNG tanker movements through the Strait of Hormuz and easing concerns over future supply disruptions weighed on prices, before rebounding this week on renewed tensions in the Middle East.

Economic Environment

• Global stocks rose in June as markets welcomed an interim agreement between the US and Iran to end the conflict and reopen the Strait of Hormuz, sending oil prices to their lowest level since late February.

• The UK's private sector remained in contraction in June, with the Composite PMI slipping to 49.4 as weaker services activity weighed on output. The data reinforce expectations of further BoE rate cuts later this year.

• German consumer confidence stabilised for July but remained subdued. While stronger income expectations provided some support, weak willingness to spend and elevated savings continued to reflect persistent economic uncertainty.

Oil

• Oil prices have fallen to their lowest level since late February as shipping through the Strait of Hormuz starts to normalise. Despite ongoing tensions, the recovery in Gulf exports has eased supply concerns, with Brent crude trading within a $27.50/bbl range during the month before ending nearly 22% lower.

• Reflecting the improved supply outlook, Goldman Sachs has lowered its Q4 2026 Brent forecast to $80/bbl from $90/bbl and reduced its 2027 average price forecast to $75/bbl from $80/bbl. The bank now expects Gulf oil exports to return to pre-conflict levels by the end of July, one month earlier than previously anticipated.

Gas

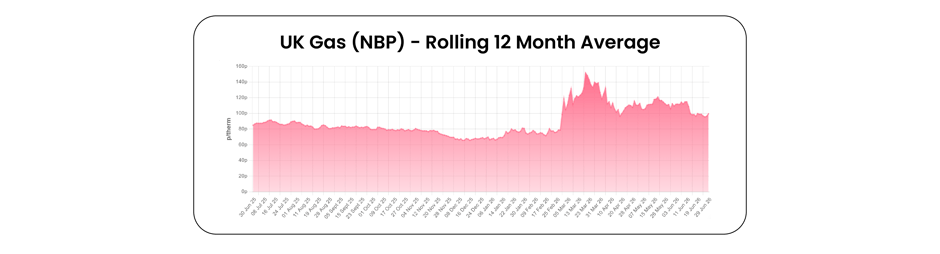

• Despite the disruption to LNG exports from Qatar over the past three months, European gas storage injections have remained resilient, with inventories rising by 9.2 percentage points over the past month to 48.6%. Injection rates should accelerate over the summer, assuming Qatari exports gradually normalise.

• According to a source familiar with the matter, QatarEnergy is prepared to restart LNG production at Ras Laffan at short notice and could return to full output within a month, excluding the two damaged trains. The key challenge will be shipping and logistics, particularly how quickly the company can secure vessels and resume cargo loadings once the Strait reopens, the source added.

• Germany's Stade floating LNG terminal (4.7bcm/year) is set to begin operations in September after repeated delays from its original 2024 launch date. Meanwhile, the 13bcm/year onshore LNG terminal at Stade has been delayed until 2029, from a previous target of end-2027. Germany currently has four floating LNG terminals in operation, with the total expected to rise to six once all planned projects come online.

Power

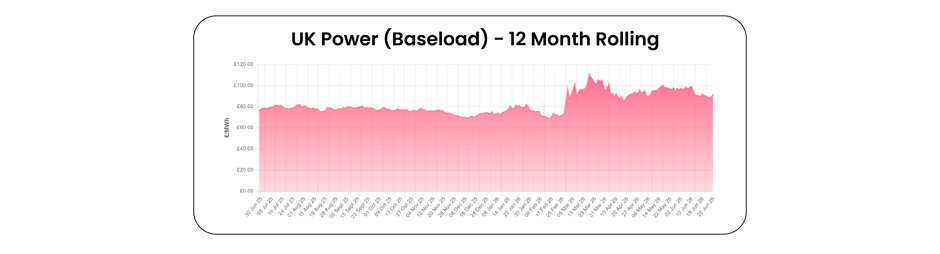

• A summit to finalise the linking of the UK and EU Emissions Trading Systems has been postponed following the UK prime minister's resignation. The UK government said it would seek to hold the summit at the earliest opportunity, with EU Council president Antonio Costa confirming the delay was necessary after Starmer's resignation.

• Short-term power markets across Europe have remained elevated this month, supported by the second heatwave of the summer, which has boosted cooling demand while reducing nuclear availability in France and Switzerland as environmental restrictions on river water temperatures have constrained reactor cooling.

• Germany's BNA regulator has scheduled two auctions for a total of 9 GW of new gas-fired generation capacity, with 4.5 GW to be tendered on 8th September and a further 4.5 GW on 22nd December. A separate 2 GW auction open to all generation technologies is planned for 18th May. Additional capacity auctions are expected in 2027 and 2029, although volumes have not yet been specified.

• While oil prices fell sharply over the month, the Winter 26 baseload power contract proved more resilient, declining by a more modest 4.3%, supported by strength in prompt power markets. The contract traded within a c. £12.3/MWh range during the month.

If you would like the latest insights weekly, sign up for our Energy Market Update.

Short-term gas prices weakened this week, with the UK day-ahead gas contract down around 10p week-on-week as heatwave conditions suppressed heating...

1 min read

Gas and oil markets have been extremely volatile this week. For example, the UK April gas contract reached 171.00 p/th on Tuesday morning, more than...

Gas prices have been volatile in recent weeks, with the February contract reaching a high of 113.00 ppt in late January. The rally was driven by...